In October 1989, a 7.1-magnitude earthquake now known as “the little big one” shook northern California just as Oakland and San Francisco were starting Game 3 of the World Series. The double-decker Nimitz Freeway in Oakland buckled and collapsed, killing 41 of the 63 people who died in the quake.

In the following weeks, the New York Times investigated the questions on many people’s minds — did California officials know the freeway wouldn’t survive a strong earthquake? Should they have known or at least suspected it? If its integrity was suspect, why were actions not taken to strengthen or close it down? The investigation exposed both structural deficiencies and political delays that contributed to what may have been a preventable disaster.

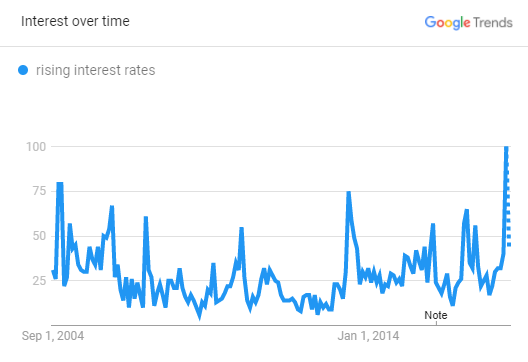

While it was impossible to know ahead of time exactly how each structure and roadway would respond to a major earthquake, state officials had been warned about the general risks and failed to take proper precautions. Similarly, we’ve heard rumblings several times in the last decade that interest rates were on the cusp of rising from their near-zero recessionary levels, but it’s actually starting to happen now. In February, Google searches for “rising interest rates” hit the highest level since 2004. The borrowing, lending, investing public senses change is afoot.

Interest rates are, at their simplest, the price of money, so the potential ripple effects from rising rates will reach across the financial markets. But let’s focus on the epicenter — fixed income. It’s common knowledge that bond prices move inversely with interest rates, but factors like maturity date, issuer leverage, or industry exposure all influence how exposed a particular bond, company or sector is to interest rates. So which parts of the market are most vulnerable today, and what can you do to shore up your clients’ portfolios?

For starters, net leverage for the median S&P 500 company is at 1.6x, the highest level in more than 40 years, fueled by the low cost of issuing and carrying debt over the last decade. The headline leverage number is well off its historic highs, but the weighted average is skewed lower by the high concentration of cash among a few of the biggest and highest-quality borrowers in the index (think Amazon, Microsoft, Apple, Google, and Berkshire Hathaway). BBB issues also make up a growing share of the investment-grade mix as large caps have levered up to fund buyback programs and M&A.

While investment-grade companies have partaken in the cheap debt buffet and will feel some financial indigestion from rising rates, they aren’t likely to become distressed even if we were to see simultaneously higher rates and deteriorating economic conditions.

The same can’t be said of high-yield issuers, however, most of which are small-cap companies. From both an interest rate risk and a credit risk perspective, the US high-yield corporate debt market looks as risky as it has in years. These metrics should act as red flags for investors:

1. Historically high small-cap leverage.

One of the prevailing narratives in the last few years is that U.S. companies have been stockpiling large amounts of cash, thereby reducing their liquidity risk. While factually accurate, this misses the fact that corporate debt has been growing much faster than corporate cash. Russell 2000 net leverage, which compares debt in excess of a company’s cash on hand to its EBITDA, is now 4.5x, as shown below juxtaposed against weighted average total debt. That’s the highest level in the last 25 years, with the exception of early 2016, when small-cap profits dropped suddenly, temporarily inflating the ratio to over 6x Even more alarmingly, 14.6% of the S&P 1500 don’t generate enough operating income to cover their interest expense as of the fourth quarter of 2017, up from 12.2% a year earlier and 5.7% 10 years earlier at the start of the Great Recession, according to Bianco Research.

Different business models and industries can carry varying debt loads, but I would venture to say that for the typical small-cap company, 4.5 times EBITDA is an unsustainable amount of leverage and could pose a threat to its financial stability when the business cycle inevitably turns downward.

Consider also the limitation on business interest deductibility in last year’s tax reform. Net interest expense above 30% of adjusted taxable income (ATI) is no longer deductible for most businesses with more than $25 million in revenue. ATI, as defined in the legislation, is roughly equivalent to EBITDA from 2018-2021, but it will automatically change in 2021 to include depreciation, amortization and depletion, making it closer to EBIT. In most cases, this will mean companies hit the 30% cap sooner and won’t receive a tax benefit from any additional interest expense.

According to FactSet, Russell 2000 companies are already spending a third of their EBIT on interest. So while there is a little breathing room under the short-term ATI definition, once it resets lower small caps will already be maxing out their interest deductions even if debt and interest rates stay at today’s levels. As Moody’s recently put it, tax reform will likely be a net negative for highly leveraged small caps. “Loss of interest deductibility will result in lower cash generation, especially among companies rated single-B and lower, weakening their ability to service high interest costs and so also shrinking their refinancing opportunities.”

2. High mix of floating-rate debt.

According to Goldman Sachs research, 42% of debt held by Russell 2000 companies is floating rate, compared to only 9% for the S&P. While companies with only fixed-rate debt won’t feel the pressure of rising interest rates on their bottom line until they refinance, floating-rate borrowers will see an immediate drop in earnings and cash flows. Libor (3-mo. USD), the most popular reference rate for such loans, has been accelerating and at the end of February broke through 2%, a level not seen since 2008. For companies that don’t fully hedge their rate exposure, interest expense could start ticking up noticeably in Q1 earnings.

We’ve heard rumblings several times in the last decade that interest rates were on the cusp of rising from their near-zero recessionary levels, but it’s actually starting to happen now, and the potential ripple effects from rising rates will reach across the financial markets.

In my last column, I talked about two red flags for fixed income investors. Here are three more signs that a seismic shift in the bond markets is coming:

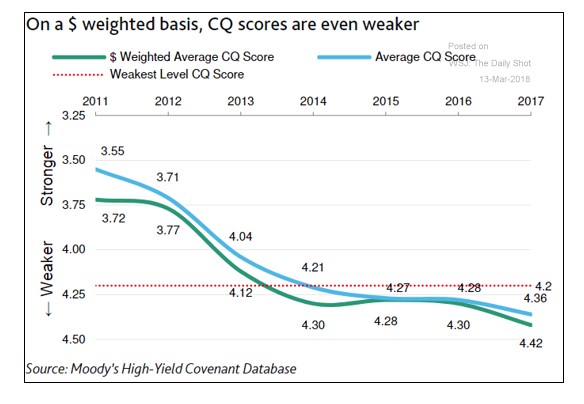

3. Weak covenant quality.

A direct byproduct of low rates has been the flood of yield-chasing money into the junk bond market, making it easier than ever before for speculative companies to borrow. Not only has new debt been cheap to issue, but bondholders haven’t demanded the same level of protection they did historically, making the credit market more vulnerable in an economic downturn.

Creditor protections, as measured by the Moody’s Covenant Quality Score, have deteriorated in five of the last six years and stand near the worst levels on record. In 2017, bonds with the weakest level of protections represented 65% of the issues Moody’s tracks, up from 23% in 2011. In January, a Moody’s vice president commented, “Borrowers are making the most of a wide-open loan market. As demand continues to outpace supply and pressure on covenant quality remains intense, it is hard to see what investors get in return for giving up covenants in these frothy market conditions.”

4. Unusually low default rates.

In the last 3-4 years, high yield default rates have uncoupled from their historical relationship with overall debt levels. As 13D Research put it, “For roughly three decades, U.S. nonfinancial corporate debt as a percentage of U.S. nominal GDP and the high-yield default rate moved in tandem. It was a logical relationship — more debt meant more defaults. However, the lowest interest rates in human history broke that correlation, and today, the divergence remains near its post-crisis extreme.”

As the Fed begins to raise rates and unwind its bloated balance sheet, one would think investors would be cautious. But the combination of placid credit conditions and better yields than the paltry 2-3% paid by many investment-grade bonds has created a false sense of security for enthusiastic buyers, which leads to our final red flag.

5. Tight credit spreads.

In the decade-long reach for yield, money has flown into longer-duration and lower-quality debt with little regard for the underlying risks. The aforementioned historically high leverage, exposure to floating rates and weak covenant quality notwithstanding, corporate bond yields have been tightening to near record lows over risk-free Treasuries as competing buyers demand less and less compensation for taking credit risk. Bonds in the ICE BofAML high-yield index are yielding an average of just 3.7% more than comparable Treasuries, up from a post-crisis low of 3.2% at the end of January.

Bond funds, especially passive ones, have driven much of the demand for new debt over the last decade. Federal Reserve data shows that mutual funds and ETFs have gone from owning just over 6% of the corporate bond market at the end of 2008 to almost 20% at the end of 2017. Over the same period, passive products have more than doubled as a share of total taxable bond fund assets, according to Morningstar data.

There are two problems with passive and marginally active funds driving an increasing share of bond buying. Like equity index funds, the underlying buyers are inherently price-insensitive. But unlike equity index funds, which are weighted by market cap and are thus skewed toward larger and ostensibly higher quality companies, bond indexes are weighted by the amount of debt issued. As a bond indexer, you’re lending the most money to the companies that issue the most debt, leaving the index skewed toward issuers with the most leverage.

In aggregate, we think investors in high-yield bonds today are being poorly compensated for risks in the next several years. We agree with the Bloomberg columnist Nir Kaissar, who said, “For that to change, high-yield bond markets will have to become a lot scarier than they have been in recent weeks.”

Silver Lining

It’s not all dark clouds on the horizon, though — savers in money markets and CDs will benefit from rising rates, as will patient buyers of high-quality bonds. While bond prices and interest rates are inversely related in the short run, starting yield is also the single best predictor of future long-term bond returns. The same Bloomberg piece showed a high correlation between starting yields and subsequent 5- and 10-year returns for both high-yield and emerging market bonds.

This makes intuitive sense — assuming no defaults, a 10-year bond purchased at a 2% yield to maturity will, by definition, average 2% nominal returns over the next decade despite any intervening price fluctuations, while the same bond purchased after a rise in rates at a 6% starting yield and held to maturity will average 6% nominal returns. As rates return to more “normal” levels (a nebulous concept, but materially higher than 0%) and the underlying risks in the bond market are exposed, I think we’ll begin to see a return to more rational risk/return dynamics, as well as significant mispricing opportunities.

The best advice I can give my fellow fixed income investors is to know what you own. Whether it’s individual issues or a bond ETF, take the time to understand the underlying credit and interest rate risks. Avoid long-duration assets if your portfolios can’t tolerate significant volatility. Stay clear of highly levered companies that will be most heavily impacted by the end of cheap debt. When the fault lines shift and the ground starts to shake, make sure your investments are already firmly anchored.

Reprinted with permission from the April 11 & April 16, 2018 issues of ThinkAdvisor. ©2018 ALM Media Properties, LLC. Further duplication without permission is prohibited. All rights reserved.